Advertisement

Help Keep Boards Alive. Support us by going ad free today. See here: https://subscriptions.boards.ie/.

https://www.boards.ie/group/1878-subscribers-forum

Private Group for paid up members of Boards.ie. Join the club.

Private Group for paid up members of Boards.ie. Join the club.

Hi all, please see this major site announcement: https://www.boards.ie/discussion/2058427594/boards-ie-2026

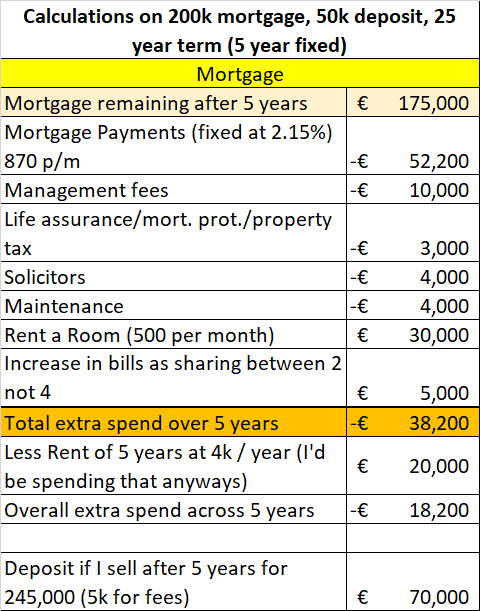

Is buying a primary home and renting out a room tax free a no lose situation?

-

09-01-2022 07:10PM#1

Comments

-

-

-

-

-

-

Advertisement

-

-

-

-

-

-

Advertisement

-

-

-

-

-

Advertisement