Advertisement

If you have a new account but are having problems posting or verifying your account, please email us on hello@boards.ie for help. Thanks :)

Hello all! Please ensure that you are posting a new thread or question in the appropriate forum. The Feedback forum is overwhelmed with questions that are having to be moved elsewhere. If you need help to verify your account contact hello@boards.ie

Hi all! We have been experiencing an issue on site where threads have been missing the latest postings. The platform host Vanilla are working on this issue. A workaround that has been used by some is to navigate back from 1 to 10+ pages to re-sync the thread and this will then show the latest posts. Thanks, Mike.

Hi there,

There is an issue with role permissions that is being worked on at the moment.

If you are having trouble with access or permissions on regional forums please post here to get access: https://www.boards.ie/discussion/2058365403/you-do-not-have-permission-for-that#latest

There is an issue with role permissions that is being worked on at the moment.

If you are having trouble with access or permissions on regional forums please post here to get access: https://www.boards.ie/discussion/2058365403/you-do-not-have-permission-for-that#latest

So a Memestock was my first Stock. What Now?

-

03-02-2021 12:24am#1Like many people, I jumped on the Gamestop rocket-ship last week. Before this I had never dabbled in the stock market or really knew anything about it. Over the last week though I have had many questions and thoughts about what to do next (to be clear, I don't mean jumping on another stock, I'm talking about practical things!) so I have been reading and researching as much as I can. I know there is a beginners thread for questions but I think this is a pretty unique situation, so I thought it might be useful to some to share what I have researched and found out. Others can add or take away as they see fit, and correct any errors, of which I am sure there will be a few!

To start things off I'll put forward a number of the main scenarios people might find themselves in, with some suggested next steps.

Scenario 1: I have sold all my stock and made a profit. This was a one time deal for me and I have no interest in doing anything more with stocks.

First off, if you are in this situation, well done! Congratulations on making some money. Before you go off spending it there are a few things to consider.

Capital Gains Tax (CGT).

Regardless of how much (or little) profit you made you will still need to make a return to Revenue regarding this by the 31st October 2022.

There is a personal exemption of €1,270. This means if you made a profit (i.e. sale price minus what you paid) of less than this you will not need to pay any CGT. However, you will still need to include this in your return next year. If you made more than the exemption you will need to pay CGT of 33% on anything above €1,270. (i.e. don't include the first €1,270 when calculating.). If you paid commission etc. on the transactions you can deduct them also. You must pay this CGT by December 15 2021 (this year!). You will not need an accountant or anything to do this, it is a very straightforward calculation, loads of detail on the Revenue website and on ROS and you can ring them too for help.

Scenario 2: I have sold all my stock and have made a loss. This was a one time deal for me and I have no interest in doing anything more with stocks.

Sorry to hear this, you are not the only one and I hope it wasn't too much money. But before you can put this all behind you there is one more thing. I discussed CGT above. Obviously you won't have to pay anything, but you should still make a return next year even if it was pocket money. Don't forget. If you sold these stocks within 4 weeks of their purchase you cannot offset the loss against any future Capital Gains as per Revenue rules:

If you have sold your stocks at a loss after holding them for a period longer than 4 weeks, you can offset the loss against future gains.Shares sold within four weeks of acquisition

If you sell them after holding them for longer then 4 weeks you can offset the loss in future.

Shares bought and sold within a four-week period cannot be offset against other gains.

You can only deduct the loss from a gain made on a subsequent disposal of same-class shares acquired within the four weeks.

Scenario 3: My stocks have tanked but I am still holding! But I have no interest in doing anything more with stocks.

Never give up hope! You have not made any losses (or gains) until you crystalize it by selling. Once you have sold, look at scenario 1 or 2 and proceed accordingly. In the mean time, as long as you have diamond hands you don't have to do anything further, although, in the unlikely scenario that company issue and you receive dividends you will have to declare this as income. This is extremely unlikely to happen so don't worry about it, and if it does it is easy to sort.

Scenario 4: I have made a profit/loss/holding but I want to continue investing with stocks.

Personally, I am still holding my GME but look like making a loss. However, I want to continue investing, but properly this time. Before we get around to that though, we still need to keep Revenue in mind going forwards. The detail I gave above still applies, however it gets more complicated with more buys and sells. I will not go into more complicated CGT stuff here like the 4 week rule, but I will say that record keeping is vital. Do not rely on any broker or institution to keep records for you. Keep your own too.

Going forward though there are a few things to keep in mind (certainly I need to!)- The Gamestop situation was unique and may never happen again, It is certainly not the norm.

- I was basically gambling here, on a sport I know nothing about. Like the aul one in the office who picks a horse in the grand national because the name sounds cool.

- I was using what random people on reddit were saying as financial advice. Sure, it may have worked out well for some, but it is certainly not a sound strategy going forward.

- Before risking any more money I need to learn more and decide on what my goals and strategy will be.

30

Comments

-

I'm in a similar boat. Have been holding crypto (and mining) for years but that's the limit of knowledge. GME was my first foray into stocks. I made a modest loss but didn't put in anything I wasn't ready to lose. I learnt an awful lot regardless. I'll be coming into a bit of money soon so am interested in putting some into something safe and stable.0

-

Good thread, on Scenario 2 however, you can't use that loss. You have to hold a stock for more than 30 days to allow it as a loss. It's something Irish Revenue put in a while back to deter people from day trading0

-

Thanks, I think you are right there, I'll edit it. You can only use that loss against gains made with the same stock within the four weeks. That's ridiculous.Good thread, on Scenario 2 however, you can't use that loss. You have to hold a stock for more than 30 days to allow it as a loss. It's something Irish Revenue put in a while back to deter people from day trading

In that case if you are in a scenario where you have already lost 'more' than the stocks are worth now you may be best advised not to crystalize any loss for four weeks so you can offset the entirety of the loss against a future gain.Shares sold within four weeks of acquisition

Shares bought and sold within a four-week period cannot be offset against other gains.

You can only deduct the loss from a gain made on a subsequent disposal of same-class shares acquired within the four weeks.0 -

0

-

Can I afford to invest, and if so, how much?

From reading around it would seem that the first thing to consider is if I can afford to invest at all, and if I can, how to decide on a budget. I've read quite a bit (again these are personal thoughts based on what I have read and could all be wrong!) and I will try at presenting my thoughts and what I have learned in a conversation style based on what I was asking myself. Some of this will depend and vary on what type of investing you are doing, but more on that later.

I have savings, shouldn't I just invest all of this because it is not earning anything in my savings account?

No, do not do this. This is a bad idea for a number of reasons. Firstly, you do not know what you are doing yet and may lose it all. Even if you did have a good idea as to what you are doing, it could still go wrong and you could lose it.

You should not invest any money you will need in the next year. Lets say you are saving for a car or a house and plan to buy in the summer. If you put all this into stocks you may lose it, or you might have to sell your stocks at an inopportune time in terms of the market. Imagine you had to spend this money last March and you had it tied up in stocks, and had to sell you stocks at the start of covid? You would have lost loads.

So to avoid this you should not invest money that you plan to spend on something specific in the next 12 months. You should also try and have a rainy day fund in cash to support you for 3/6 months. You do not want to have everything tied up in stocks forcing you to have to sell them, perhaps at an inopportune time, to pay for an unexpected bill.

But the whole point of why I want to invest is because I have little money and I have debt I want to clear!

In a future post I will go through the goal options I looked at what I am thinking about doing myself and how I have decided. But for now, it is sufficient to say that you should not invest money until you have sorted your own personal finances out. If you do not have the discipline in this area, how can you expect to be a success at investing? You need to get your personal finances in order and have a budget. There are plenty of things out there that can help you. Have a look at your incomings and outgoings and categorize them all so you know exactly what you are spending week to week and month to month and on what.

After you have done that you need to try and work out if you are overspending. Some items might be obvious, others no so much. One resource that is especially helpful in an Irish context is the 'Reasonable Living Expenses' calculator offered by the Insolvency Service of Ireland. Details on this can be found here and a calculator that you can put details into is available here: https://backontrack.ie/rle-calculator/

To explain, the RLE's are a calculation that the government use to calculate how much money you need to have a "reasonable" lifestyle. They use this for people who are insolvent or are declared bankrupt. It is a "frugal" calculation but a realistic one too, many people are forced to live by these figures. There is a space for "Special Circumstances" be sure to only put stuff in here that you think is strictly necessary (say if you have ongoing medical expenses, car loan repayments etc.), not stuff like Netflix. Once it gives you a figure, subtract this from your net income. The RLE's are a bit frugal so you may want to add a little extra on to them depending on your circumstances. This should all help you to see if you are overspending and will enable you to adjust accordingly.

If you have any remaining money after all this, you need to decide how to split this between investment money, clearing any debt and savings. Personally I would be inclined to get rid of any high interest debt like credit cards first, then work on getting savings to a level as previously discussed and finally investment money. You might look at splitting the money 80/20 between savings and investment money and adjusting this ratio as time goes by.

I've done this and I have no money left over!

If you have no money whatsoever left over after doing all the sums and being strict with your spending, I'm afraid you can't really afford to invest currently. You do not want to be taking money you need for bills and investing it hoping to make a quick profit. It probably won't work, and it is not fair on you and your family. You need to identify ways either to earn more money or to reduce expenses. But don't give up, please read on. You can still learn about everything so when you can afford it, you are ready.

I have done all my budgeting and I have decided I can afford to invest, lets go!!

Not so fast. Rushing in is a good way to lose your money. They only thing you know at this stage is that you have some money that you can reasonably, and responsibly, afford to invest. You still don't know what you are doing.

Regardless of whether you can currently afford to invest or not your next steps are the same. You need to learn about the market, decide on a realistic goal, and decide on an investment strategy and style. I'll go through my thinking on these topics in future posts.

(Again just to reiterate I'm a complete newbie to all of this and an experienced person might think I'm talking rubbish, but these are my thoughts and approach to it, mileage may vary etc.)0 -

Advertisement

-

Just to add to the above so people know where I am at, I am in a position where I can afford to invest some money.0

-

Well done on.this thread.

If I might suggest:

1. You say don't invest if you need the money in next 12 months. That's a good starting point, but even at that period you're carrying quite a bit of risk that it will be worth less than when you started. A 10-20 year horizon gives you a better chance but still doesn't guarantee positive return, based on historical performance

2. Something like 95% of professional investment managers do not manage to beat the average total market return over 5-10 years. If someone wants to make money in the stock market, the best option for most is to buy an index product and hold it. Boring yes, but statistically a good approach.

3. If you want to day trade, you're playing in a game rigged against you in favour of the pros/institutions. You don't know the rules, you can't play when they play and you have to tell them your move before you can make it and give them time to decide if they want to take advantage of it. Don't use traditional Irish brokers if you want to day trade unless you're moving very large amounts, the commissions will eat all your profit.

4. A monkey throwing darts would have made good money picking stocks in the last decade, including 2020. Don't expect those market conditions to last forever. Don't invest money you can't afford to lose.

5. ETFs tracking an index are a good approach re number 2 above, except they are punitively taxed in Ireland. Despite that, an Accumulating ETF isn't awful from a tax perspective for the long term holder (with the hope that a long term hold means I don't have losses so don't lose out in terms of not being able to offset those losses on ETF against gains on other investments.

6. Stock picking can be fun if you view it as entertainment with a potential for making money.0 -

Great points.PaddyTheNth wrote: »Well done on.this thread.

If I might suggest:

1. You say don't invest if you need the money in next 12 months. That's a good starting point, but even at that period you're carrying quite a bit of risk that it will be worth less than when you started. A 10-20 year horizon gives you a better chance but still doesn't guarantee positive return, based on historical performance

2. Something like 95% of professional investment managers do not manage to beat the average total market return over 5-10 years. If someone wants to make money in the stock market, the best option for most is to buy an index product and hold it. Boring yes, but statistically a good approach.

3. If you want to day trade, you're playing in a game rigged against you in favour of the pros/institutions. You don't know the rules, you can't play when they play and you have to tell them your move before you can make it and give them time to decide if they want to take advantage of it. Don't use traditional Irish brokers if you want to day trade unless you're moving very large amounts, the commissions will eat all your profit.

4. A monkey throwing darts would have made good money picking stocks in the last decade, including 2020. Don't expect those market conditions to last forever. Don't invest money you can't afford to lose.

5. ETFs tracking an index are a good approach re number 2 above, except they are punitively taxed in Ireland. Despite that, an Accumulating ETF isn't awful from a tax perspective for the long term holder (with the hope that a long term hold means I don't have losses so don't lose out in terms of not being able to offset those losses on ETF against gains on other investments.

6. Stock picking can be fun if you view it as entertainment with a potential for making money.

My personal approach will be that any money I invest will be low and will not be 'needed' for anything and can either all be lost (hopefully not) or left there indefinitely.

In my personal budgeting I have identified a number of hobbies that I only spend money on out of habit, rather than actually enjoying them. I spent a lot of time and money on gaming previously, but I don't really spend that much time at it anymore but I still buy a good few games every year as well as online subscriptions. I used to blame a lack of time for why I didn't play much and never completed games, but I have not turned on my PlayStation bar a handful of times during Covid even though I have loads of free time. So the reality is that I'm just not interested in gaming anymore. So I have cancelled my subscriptions and will not be purchasing any new games or consoles. I was surprised when I averaged out how much I was spending on a monthly basis, it was quite a bit.

So through this and some other items I have identified a few ways that I am basically wasting money. My aim is to spend this money instead on investing. By doing it this way, I am not actually interrupting my normal budget or savings plans, but rather I am just spending some of my "hobby" money on something different - investing. This seems to me, in my personal circumstances, a prudent approach.0 -

Right, so lets start learning then.

Many people on here have recommended the "MyWallStreet" 'Learn' app which is available on your smartphone. This is free, and I found it a useful introduction. So I'd recommend starting there. You can also access it on your desktop (for free) here: https://learn.mywallst.com/

As for further recommendations on where to go to learn more and to find good resources, I don't really have any I can stand over. As I said, I'm totally new to this too. But I have done a lot of Googling and reading of what other people "suggest" as good websites and resources. Some of these "suggestions" were blatantly paid for advertorials so I ignored them, but I have compiled a series of links that may be useful. However, I do need to stress that I have not used the sites and cannot vouch for their usefulness. The reason why I am posting is that it may save others from spending ages like I have sifting through recommendation posts, threads and articles. My criteria was strict in that all the sites are either free, or have a free version which is still useful. Don't go paying for anything yet! The sites also had to be recommended multiple times over the course of my 'research'.

Here they are in no particular order:

https://www.investopedia.com/

https://docoh.com/

https://www.wallstreetoasis.com/forums/on-the-job-with-simple-as-my-research-process

https://finance.yahoo.com/

https://finviz.com/

https://www.sec.gov/

http://openinsider.com/

https://seekingalpha.com/

https://www.tradingview.com/

https://wallmine.com/market/us

https://whalewisdom.com/

http://finra-markets.morningstar.com/BondCenter/Default.jsp

https://www.investing.com/

https://www.insidertracking.com/

https://eresearch.fidelity.com/eresearch/markets_sectors/sectors/si_performance.jhtml?tab=siperformance

https://www.marketwatch.com/

https://www.stockconsultant.com/consultnow/basicplus.cgi

http://www.stockta.com/

https://simplywall.st/about

https://www.morningstar.com/

https://hindenburgresearch.com/

https://stocktwits.com/

Obviously this list is not exhaustive, and as said some of the sites may be rubbish so hopefully more experienced people here can add and take away. Anyway I hope the above may prove useful to some of you and save you from the chore of sifting through recommendation lists (or at least give you a head start!).

Personally, I next want to find some books and reliable educational people on Youtube so if anyone has recommendations that would be great.0 -

Good thread, on Scenario 2 however, you can't use that loss. You have to hold a stock for more than 30 days to allow it as a loss. It's something Irish Revenue put in a while back to deter people from day trading

What? That has me quite worried considering I submitted my return on some very different assumptions.

That has me quite worried considering I submitted my return on some very different assumptions.

You're saying that if I buy 10 GME shares today and sell them tomorrow (never buying them back) at a loss of €1000, that I cannot use that to offset my overall gains on other stocks?

My understanding was that the only preclusion was on buying back within the 4 weeks i.e. if I bought 10 GME today, sold tomorrow at a loss of €1000, and then bought back the day after that, I could not the €1000 loss in my calculations of CGT on, say, Bank of Ireland shares.

Taken from the Revenue handbook:

"Furthermore, where a loss accrues on the disposal of shares and shares of the same class are acquired within a four week period, the loss is not available for offset against any other gains arising. Instead the loss is only available for set off against any gain that might arise on the subsequent disposal of the shares so acquired in the four week period - this provision does not apply where there is a gain on the disposal."

Am I misreading this or has the law changed?0 -

Advertisement

-

Shares sold within four weeks of acquisitioninisfree0504 wrote: »What? That has me quite worried considering I submitted my return on some very different assumptions.

You're saying that if I buy 10 GME shares today and sell them tomorrow (never buying them back) at a loss of €1000, that I cannot use that to offset my overall gains on other stocks?

My understanding was that the only preclusion was on buying back within the 4 weeks i.e. if I bought 10 GME today, sold tomorrow at a loss of €1000, and then bought back the day after that, I could not the €1000 loss in my calculations of CGT on, say, Bank of Ireland shares.

Taken from the Revenue handbook:

"Furthermore, where a loss accrues on the disposal of shares and shares of the same class are acquired within a four week period, the loss is not available for offset against any other gains arising. Instead the loss is only available for set off against any gain that might arise on the subsequent disposal of the shares so acquired in the four week period - this provision does not apply where there is a gain on the disposal."

Am I misreading this or has the law changed?

Shares bought and sold within a four-week period cannot be offset against other gains.

You can only deduct the loss from a gain made on a subsequent disposal of same-class shares acquired within the four weeks.- Example 2 On 1 April 2017, both Jane and Kevin individually bought 3,000 ordinary shares in Abcee Ltd for €3,000.

They both then sold their shares on 14 April 2017 for €2,000, making a loss of €1,000.

Jane did not buy any more ordinary shares in Abcee Ltd within four weeks making the loss. She cannot set her loss against any gain she may make.

Kevin bought more ordinary shares in Abcee Ltd on 21 April 2017. If Kevin makes a gain on the disposal of these shares in the future, he can deduct his loss of €1,000.

0 - Example 2 On 1 April 2017, both Jane and Kevin individually bought 3,000 ordinary shares in Abcee Ltd for €3,000.

-

What you have there is in the context of FIFO I believe.inisfree0504 wrote: »What? That has me quite worried considering I submitted my return on some very different assumptions.

You're saying that if I buy 10 GME shares today and sell them tomorrow (never buying them back) at a loss of €1000, that I cannot use that to offset my overall gains on other stocks?

My understanding was that the only preclusion was on buying back within the 4 weeks i.e. if I bought 10 GME today, sold tomorrow at a loss of €1000, and then bought back the day after that, I could not the €1000 loss in my calculations of CGT on, say, Bank of Ireland shares.

Taken from the Revenue handbook:

"Furthermore, where a loss accrues on the disposal of shares and shares of the same class are acquired within a four week period, the loss is not available for offset against any other gains arising. Instead the loss is only available for set off against any gain that might arise on the subsequent disposal of the shares so acquired in the four week period - this provision does not apply where there is a gain on the disposal."

Am I misreading this or has the law changed?0 -

I'm not a tax consultant but that's my understanding of it and how I do my returns.inisfree0504 wrote: »What? That has me quite worried considering I submitted my return on some very different assumptions.

You're saying that if I buy 10 GME shares today and sell them tomorrow (never buying them back) at a loss of €1000, that I cannot use that to offset my overall gains on other stocks?

I calculate all the sells that I've made a loss on, then figure out which were sold within 30 days, and exclude those.0 -

Lamar Thoughtless Napkin wrote: »Shares sold within four weeks of acquisition

Shares bought and sold within a four-week period cannot be offset against other gains.

You can only deduct the loss from a gain made on a subsequent disposal of same-class shares acquired within the four weeks.

[*]Example 2 On 1 April 2017, both Jane and Kevin individually bought 3,000 ordinary shares in Abcee Ltd for €3,000.

They both then sold their shares on 14 April 2017 for €2,000, making a loss of €1,000.

Jane did not buy any more ordinary shares in Abcee Ltd within four weeks making the loss. She cannot set her loss against any gain she may make.

Kevin bought more ordinary shares in Abcee Ltd on 21 April 2017. If Kevin makes a gain on the disposal of these shares in the future, he can deduct his loss of €1,000.

It is correct that the loss on shares sold within 4 weeks is lost unless it is used against the gain made on the same shares. I bought NAKD for €1.90 and the price went down the minute I bought them. I can’t sold them now to recover some money so I can use the loss against other gains. I have to wait at least 4 weeks. I hope to make a profit on other shares above personal exemption of 1270 enough to cover the loss and use the exemption.

Thanks Ex loco refugii for this thread ... I am a newbie on stocks too0 -

Using this example, what if I bought gamestop stock at €50 and sold 3 weeks later for €400 and reinvested all into crypto that same day to hold. Does CGT still apply for reinvestment?0

-

baron von something wrote: »Using this example, what if I bought gamestop stock at €50 and sold 3 weeks later for €400 and reinvested all into crypto that same day to hold. Does CGT still apply for reinvestment?

Yes unfortunately0 -

baron von something wrote: »Using this example, what if I bought gamestop stock at €50 and sold 3 weeks later for €400 and reinvested all into crypto that same day to hold. Does CGT still apply for reinvestment?

If you sell for a loss within 4 weeks, you can't use that loss for CGT purposes.

The CGT is due on the Crypto is completely new transaction0 -

baron von something wrote: »Using this example, what if I bought gamestop stock at €50 and sold 3 weeks later for €400 and reinvested all into crypto that same day to hold. Does CGT still apply for reinvestment?

Your realised gains are €350, if I'm not mistaken.0 -

Look at it this way, if you sold land and made a Capital Gain, you would not be exempt from paying tax on it just because you went ahead and spent it all on another asset, the future sale of which could possibly result in a Capital Gain.baron von something wrote: »Using this example, what if I bought gamestop stock at €50 and sold 3 weeks later for €400 and reinvested all into crypto that same day to hold. Does CGT still apply for reinvestment?

From what I have read (this forum and elsewhere) lots of people are making the mistake of thinking that they only need to pay tax when they remove cash from their broker account and are somehow exempt if they sell shares for a profit and immediately reinvest the proceeds. This approach will end in tears. This is why I have put so much emphasis on tax in this thread (more to come).

In your example you may not need to pay CGT depending on how many shares you bought, you may have profited by less than the exemption of €1,270.00. As I covered in my OP, you would still need to detail it in your return next year.0 -

Lamar Thoughtless Napkin wrote: »Look at it this way, if you sold land and made a Capital Gain, you would not be exempt from paying tax on it just because you went ahead and spent it all on another asset, the future sale of which could possibly result in a Capital Gain.

From what I have read (this forum and elsewhere) lots of people are making the mistake of thinking that they only need to pay tax when they remove cash from their broker account and are somehow exempt if they sell shares for a profit and immediately reinvest the proceeds. This approach will end in tears. This is why I have put so much emphasis on tax in this thread (more to come).

In your example you may not need to pay CGT depending on how many shares you bought, you may have profited by less than the exemption of €1,270.00. As I covered in my OP, you would still need to detail it in your return next year.

Curious where in the return exactly you put in the bit if you got under 1270 which I did last year? I'll be doing it this year and will be my first time as I never bought or sold a share before last year. The share was in Boohoo on the Frankfurt exchange if it matters which I assume it doesn't and profited around 1000. Also curious if I had 100 euro loss for example how would that be reported. Thanks a mill.0 -

Advertisement

-

There is a video earlier in this thread which covers some of this.Curious where in the return exactly you put in the bit if you got under 1270 which I did last year? I'll be doing it this year and will be my first time as I never bought or sold a share before last year. The share was in Boohoo on the Frankfurt exchange if it matters which I assume it doesn't and profited around 1000. Also curious if I had 100 euro loss for example how would that be reported. Thanks a mill.

Basically you need to register for Capital Gains Tax on ROS and you enter the details on Form 11 I think it is. I have not personally done this yet myself, if I ever get to that stage I will go through it in detail. If you do not need to do an Income Return I think the form is CG1.That said, I have been told that it is very straightforward, and the main complication is if you kept poor records and as a result struggle with the sums.

EDIT: Just to add I am not a tax expert so get proper advice/don't blame me etc.0 -

Goal Setting and Risk Appetite

I thought it might be helpful (both for me and maybe someone else in the same boat) to detail my thoughts on my personal risk appetite and goal setting process. Obviously people have different priorities, circumstances and risk tolerances, the below are my own thoughts. Again, I'm not saying I am doing this correctly so any suggestions etc. are much appreciated.

Having considered the risks involved, my personal circumstances and risk appetite I have decided that I will only invest what I can afford, with minimal impact, to totally lose. I could 'afford' to lose a lot of money without being out in the street, but my own definition of 'afford' is that should I lose everything I invest it should have no impact on my day to day life or plans. Obviously it would be upsetting, but I don't want to be in a 'having to tighten my belt' situation if everything tanks. This means that the amount of money I put in can have no impact on my day to day life either, i.e. it cannot detract from my normal savings, holidays etc. It also means that any 'goals' I can have from investing cannot be too significant in terms of my future (i.e. I can't be investing with the goal that the money will look after me in retirement). In theory this approach could give license to take great risks with any money I invest, however my approach is that although the loss of the money would not impact me, I would still rather not lose it if at all possible.

In practical terms, having done the sums, it means I will be starting off with a 'pot' of approx €500 to €1,000 and will be topping it up by €100 on a fortnightly basis. So €2,600 per year. This may increase in line with any salary increases. I am not comfortable with the exposure of using leverage, CFDs, shorting etc. so my investing will consist of buying and holding stocks, increasing my position in each regularly (i.e. 'dollar cost averaging'). I will not be day trading. The low amounts I will be starting with and adding means that I will have to utilise a broker who allows/facilitates fractional shares. I want to keep my tax affairs as straightforward as possible so I will not be investing in ETF's but I am content to manage receipt of dividends.

What I am thinking is to eventually have a fairly diverse portfolio of between 10 and 20 stocks. The money will be weighted in this order (1 being the most money, 4 the least): (1) Investment Trust PLC type stocks, (2) steady unexciting highcap companies that the trusts do not have large holdings in, (3) more risky/growth potential stock and (4) More speculative stock. The 'speculative' stock is to have a bit of craic with as a hobby but will be treated seriously in that I will only invest in something that I think has a reasonable chance at growth, i.e. not Gamestop!

My goals are long term, in that in 5/10/15/20 years time I hope to have 'earned' more money than I would have if I just stuck the €217 into a bank account each month and left it. It would be a nice little nest egg to have. I think this is a modest and realistic goal, and there is a fair chance I will 'overachieve' given my prudent approach. I also think it unlikely, if I stick to this approach, that everything would go entirely down the drain.

As I mentioned I need to use a broker who facilitates fractional shares, I have decided that Trading212 seems to be my best option to start with. They also have a 'virtual' service which I will be practicing on for a minimum of 4 weeks before using any real money.

Any feedback would be appreciated, especially if you think I am being imprudent or stupid. Obviously it depends on what stocks I pick but I'm not there yet!0 -

Hi OP I'm starting something similar to yourself, but at a lower scale of 50 a month and following the picks on Mywallst. I'm currently using revolut for investing. (Not sure if that's the right thing to do, but that's what I'm using)

I do like the Mywallst philosophy of seeing it as a long term deal, similar to a pension to (hopefully) watch grow over time.0 -

Hi OP I'm starting something similar to yourself, but at a lower scale of 50 a month and following the picks on Mywallst. I'm currently using revolut for investing. (Not sure if that's the right thing to do, but that's what I'm using)

I do like the Mywallst philosophy of seeing it as a long term deal, similar to a pension to (hopefully) watch grow over time.

I've used both Revolut and Trading 212, and I prefer the latter. It's free to sign up so you can take a gander.0 -

I will not be using revolut because the interface is quite basic, and it has a very limited number of stocks available. I'm currently on a waitlist for Trading212 which seems to be the best option for us in this part of the world for investing small sums.Hi OP I'm starting something similar to yourself, but at a lower scale of 50 a month and following the picks on Mywallst. I'm currently using revolut for investing. (Not sure if that's the right thing to do, but that's what I'm using)

I do like the Mywallst philosophy of seeing it as a long term deal, similar to a pension to (hopefully) watch grow over time.

DeGiro seems popular for larger sums, but does not allow fractional shares which you and I would need, and there are also charges.

Let me know how you get on with MyWallStreet, personally I am reluctant to sign up to any subscription service.0 -

Hi OP

Starting off here as well.

Will have €500 per month to invest. Using Trading 212.

Hope to do the following

A. Set up a PIE with 15 -20 companies mainly blue chip with a diverse range and possible 10 -15% speculative / more volatile companies Invest €300 per month into this

B. Set up a PIE with 3-5 Investment trusts in it. SCOTTISH Mortgage, Bankers Inc Trust, AllianzeTech Trust etc. Invest €200 per month into this.

Maybe this is a daft way of doing things but it saves me looking at things daily and once I'm making a few % above what it would make in the bank then happy days.

Hope to leave it there for 5 -10 years.0 -

Lamar Thoughtless Napkin wrote: »

Goal Setting and Risk Appetite

.....

€2,500 - €3,000 over 10 to 20 stocks means going no where, or down. Nobody is good enough to pick 10 or 20 solid stocks every time and even if one or tow of your stocks were to double in it would have little or no impact on your overall performance as the position would be small and the gain swallowed by the losses on the others.

Accumulate your savings and make a single purchase each year in an trust or similar US vehicle and you are more likely to do well.0 -

The theory was to eventually have up to 20 stocks, I'll be starting off with much less. The money in any case would be weighted towards the trusts, I won't have it evenly divided.€2,500 - €3,000 over 10 to 20 stocks means going no where, or down. Nobody is good enough to pick 10 or 20 solid stocks every time and even if one or tow of your stocks were to double in it would have little or no impact on your overall performance as the position would be small and the gain swallowed by the losses on the others.

Accumulate your savings and make a single purchase each year in an trust or similar US vehicle and you are more likely to do well.

I get your point though. However I don't see the advantage of making a single purchase each year rather than spreading it out over the length of the year.0 -

This seems to make a decent amount of sense to me, but what do I know!Hi OP

Starting off here as well.

Will have €500 per month to invest. Using Trading 212.

Hope to do the following

A. Set up a PIE with 15 -20 companies mainly blue chip with a diverse range and possible 10 -15% speculative / more volatile companies Invest €300 per month into this

B. Set up a PIE with 3-5 Investment trusts in it. SCOTTISH Mortgage, Bankers Inc Trust, AllianzeTech Trust etc. Invest €200 per month into this.

Maybe this is a daft way of doing things but it saves me looking at things daily and once I'm making a few % above what it would make in the bank then happy days.

Hope to leave it there for 5 -10 years.

One concern I would highlight with the "pie" approach is that if you frequently re-balance it (i.e. it automatically buys/sells to readjust to the % holdings you specify) it may get a little messy in terms of record keeping and reporting tax. When Trading212 are taking sign-ups again I will be messing around with the "virtual" facility they have to see how this works in practice to confirm my opinion but personally I am inclined to avoid the pie function for this reason.

If you have a few investment trusts I would see little point in separately holding companies who the trusts have large positions in. For example, Scottish Mortgage have a quite large TESLA holding, would not seem to make sense to have a personal holding of any decent size in it too. You would need to check all this on an ongoing basis to not expose yourself too much by having lots of overlap between what the trusts have and what you have personally.

I have not decided specifically what ITs I will be investing in, but I plan to have them as the core of my portfolio where most of the money goes. I plan to have a balance of growth orientated trusts and more value/conservative ones too.

In terms of "growth" trusts I have looked at Scottish Mortgage (SMT) but I am leaning towards its stablemate Monks which is more diverse. In particular I have a concern about TESLA and Monks holding is far less than in SMT. 20% of SMTs holdings are also in unlisted companies. SMT also has a quite concentrated "top 10" in terms of its holdings, whereas Monks is much more spread out. But then again SMT has preformed amazingly. But I am leaning towards Monks. Any opinions here much appreciated.

In terms of a more conservative trust, I have been looking at Capital Gearing, but have not researched a whole lot on this yet.

As for what number of trusts, how many is optimum? Would 2 be sufficient as a "foundation" to start off with? Last thing you want is lots of trusts who all hold the same investments themselves...0 -

Advertisement

-

Thanks for the heads up. Doing a bit if research here into the INV Trusts.Lamar Thoughtless Napkin wrote: »This seems to make a decent amount of sense to me, but what do I know!

One concern I would highlight with the "pie" approach is that if you frequently re-balance it (i.e. it automatically buys/sells to readjust to the % holdings you specify) it may get a little messy in terms of record keeping and reporting tax. When Trading212 are taking sign-ups again I will be messing around with the "virtual" facility they have to see how this works in practice to confirm my opinion but personally I am inclined to avoid the pie function for this reason.

If you have a few investment trusts I would see little point in separately holding companies who the trusts have large positions in. For example, Scottish Mortgage have a quite large TESLA holding, would not seem to make sense to have a personal holding of any decent size in it too. You would need to check all this on an ongoing basis to not expose yourself too much by having lots of overlap between what the trusts have and what you have personally.

I have not decided specifically what ITs I will be investing in, but I plan to have them as the core of my portfolio where most of the money goes. I plan to have a balance of growth orientated trusts and more value/conservative ones too.

In terms of "growth" trusts I have looked at Scottish Mortgage (SMT) but I am leaning towards its stablemate Monks which is more diverse. In particular I have a concern about TESLA and Monks holding is far less than in SMT. 20% of SMTs holdings are also in unlisted companies. SMT also has a quite concentrated "top 10" in terms of its holdings, whereas Monks is much more spread out. But then again SMT has preformed amazingly. But I am leaning towards Monks. Any opinions here much appreciated.

In terms of a more conservative trust, I have been looking at Capital Gearing, but have not researched a whole lot on this yet.

As for what number of trusts, how many is optimum? Would 2 be sufficient as a "foundation" to start off with? Last thing you want is lots of trusts who all hold the same investments themselves...0 -

This website seems useful as a starting position (if you haven't already seen it) https://www.itinvestor.co.uk/Thanks for the heads up. Doing a bit if research here into the INV Trusts.0 -

Lamar Thoughtless Napkin wrote: »Capital Gains Tax (CGT).

Regardless of how much (or little) profit you made you will still need to make a return to Revenue regarding this by the 31st October 2022.

There is a personal exemption of €1,270. This means if you made a profit (i.e. sale price minus what you paid) of less than this you will not need to pay any CGT. However, you will still need to include this in your return next year. If you made more than the exemption you will need to pay CGT of 33% on anything above €1,270. (i.e. don't include the first €1,270 when calculating.). If you paid commission etc. on the transactions you can deduct them also. You must pay this CGT by December 15 2021 (this year!). You will not need an accountant or anything to do this, it is a very straightforward calculation, loads of detail on the Revenue website and on ROS and you can ring them too for help.

Is there a joint assessment CGT credit of €2540? Or do shares need to be jointly owned to qualify for it?0 -

My understanding (*not a tax expert klaxon*) is that the €1270 is a personal exemption and cannot be transferred.Black_Knight wrote: »Is there a joint assessment CGT credit of €2540? Or do shares need to be jointly owned to qualify for it?

However, if your spouse has eligible CGT losses (after offsetting against her own gains, if any) you can offset them against a gain you make yourself.

I am not married so I have not looked into this in any great detail.0 -

Right, so after a great deal of consideration and research, this is my plan. Posting this both for feedback, and in the hope someone might get something useful out of it (in line with the aim of this thread).

What is my Goal?

My goal is simply to have gained more on what I have invested than if I just stuck it into the bank. I already have excellent pension arrangements. This money would be a "bonus" to have in the future and is separate from other "needed" funds which have/will be budgeted for accordingly. In other words, if I lose it all, while it would suck beyond belief, I would not have to cancel or rearrange life plans. I am 30 now, it would be a nice dream to have a decent "bonus" pile of cash when I am 50.

What is my timescale?

I intend to buy and hold long term, performance will be judged over the course of 5/10/15/20 years. GME has taught me that short plays are not for me, unless I want to watch tickers all day and get no work done!

How Much Will I Invest?

I am purchasing (hopefully) a new house this year so funds for the stock market will be limited. I will probably just buy a couple of hundred quids worth of each, and once I have my house bought commence sustainable regular monthly top ups going forward which will increase as time goes on, in line with my income.

What Investment Trusts/Stocks Will I buy??

I have identified 5 investment trusts and 1 stock which will be my initial holdings, in three broad categories. There is some overlap within the catagories, but the catagorisation is largely in line with the stock/trust mentality.

Defensive:

1. [URL="http://tools.morningstar.co.uk/uk/cefreport/default.aspx?SecurityToken=E0GBR004CX]2]0]FCGBR$$ALL"] (CGT) Capital Gearing Trust[/URL]

2. [URL="http://tools.morningstar.co.uk/uk/cefreport/default.aspx?SecurityToken=F0000008LG]2]0]FCGBR$$ALL"](RICA) Ruffer Investment Company Limited[/URL]

Value:

3. [URL="http://tools.morningstar.co.uk/uk/cefreport/default.aspx?SecurityToken=E0GBR00R16]2]0]FCGBR$$ALL"](AGT) AVI Global Trust PLC[/URL]

4. (BRK.B) Berkshire Hathaway Inc Class B

Growth:

5. [URL="https://tools.morningstar.co.uk/uk/cefreport/default.aspx?SecurityToken=E0GBR00PWQ]2]0]FCGBR$$ALL"](MNKS) Monks Investment Trust[/URL]

6. [URL="https://tools.morningstar.co.uk/uk/cefreport/default.aspx?SecurityToken=F000000JUY]2]0]FCGBR$$ALL"](JMG) JPMorgan Emerging Markets Inv Trust [/URL]

Each of the above are reputable organisations, all with decent records. As a group, I think it strikes a good diversification balance, although I would appreciate any opinions. I expect the Defensive 2 to protect my investment, with a good chance of modest gains. I don't think I will go too drastically wrong with the Value 2, and could make some decent gains here all going well. With the Growth 2, who knows? I was tempted to go for Scottish Mortgage but it is a bit too risky, Monks seems to be a watered down version, but still has a great record. I wanted some good exposure in emerging markets, China in particular. JP Morgan's offering seemed the best, especially as I did not want two trusts run by Baille Gifford in my portfolio.

Between the six there is some overlap in their holdings. I have tried to minimize this, but obviously I will have to keep an eye on things.

On whether I add any more stocks or trusts over time, that option remains open, but if I do it will be on a value investing style basis, and carefully considered. I will resist jumping on momentum stocks. But even if I add nothing, I think it is a decent portfolio.

What Broker Will I Use?

This was a hard one. When looking at a broker I had some strict requirements:

1. They must offer Investment Trusts.

2. They must be low cost or commission free if possible, particularly early on due to modest starting sums.

3. They must be safe and secure.

4. The should allow share transfers to other brokers.

4. Preferably, they should offer fractional shares.

DEGIRO is a very popular broker and the first one I looked at. However, they do not offer investment trusts and do not offer fractional shares. While cheap (they seem to be the cheapest of the non "zero commission" brokers) they are not free. They are very reputable, secure and allow you to move your shares to another broker.

Trading212: These are "free", allow fractional shares and offer Investment Trusts. While regulated and anything going wrong is unlikely, they are not around as long as some other "proper" brokers and some have expressed worry over what would happen to your shares if they went down the tubes (who really owns the asset, how clearly are your holdings demarcated from everyone else's etc.). This is perhaps an unlikely scenario, however a serious concern is that they do not allow you to transfer your shares to another broker, so if you decided to move you have to sell everything and move the cash, this can have serious tax implications of course. They also allow you to lodge funds from your debit card.

Etoro: Basically has the same good and bad points as Trading212.

Revolut: Similar good and bad points as T212 and Etoro, but way less stocks available, no investment trusts.

Interactive Brokers: These have investment trusts, very reputable (perhaps the most?), allow fractional, allow transfer to other brokers, but, while low cost, they are the most expensive on this list.

I have decided that long term Interactive Brokers suit me best. However, their costs (basically €10 a month minimum, perhaps more depending on number of trades) will not work for me at the start, for the first 12/18 months due to irregular/low amounts investing each month due to house purchase. So my plan is to start with Trading 212 in the beginning and then shift to Interactive Brokers after I get settled with my house, gradually if needed, in line with using my CGT allowances to avoid paying CGT. This should be easily achievable over the short term as I would not expect massive gains due to modest starting sums.

So to Conclude...

I think the above is a reasonable (dare I say sensible?) plan, with reasonable stocks, that give a good chance of decent returns over the long term and hopefully mitigates reasonably well against the risk of losing everything. Any and all opinions appreciated, I have probably missed something! Right now I am just waiting on T212 to allow sign ups again so I can get started!0 -

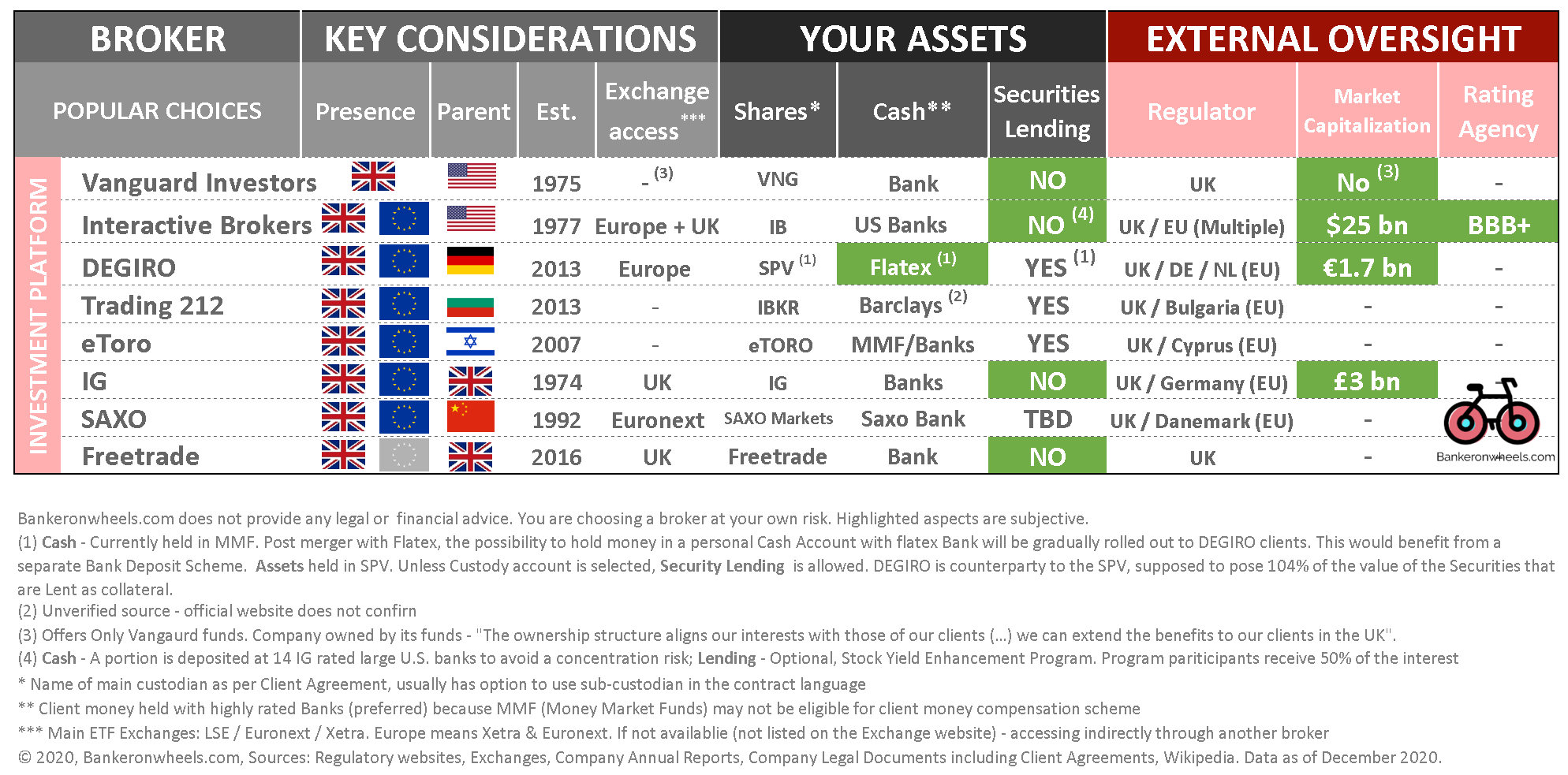

For those concerned about broker long term safety/viability, I found this article useful:

https://www.bankeronwheels.com/how-to-choose-a-safe-stock-broker/

Interactive Brokers seem to be the most secure, largely because they are the largest and most transparent, due to the fact that they are publicly traded and agency rated (the thinking being that public scrutiny should keep stuff safe/flag issues - in theory). So I think a monetarily small portfolio (under 20k, the amount covered by the Investment Compensation Scheme) with Trading212 is ok (stocks ultimately held with Interactive Brokers, but conceivably T212 could mess up something) with larger sums done directly with IB makes sense.0 -

Advertisement

-

Opened an account with Interactive Brokers today, seemed very painless, ID etc. approved in minutes. Transferred a grand in to get started (from Revolut) which may take a couple of days to reach my IB account.

Soured on Trading212, just taking too long to open to new members (guaranteed they will start accepting new members any second now!) and when I considered their FX fees, and lodgement fees (from a Card) as well as other factors discussed previously (share lending etc.) I decided to just bite the bullet and go with IB. I will let people know how I get on, it seems very good so far, oodles of information. There is an online portal for simple trades (will use this most often I'd say) and there is also a "workstation" that you download, this seems very complicated and something like you see day-traders use. There is also a mobile app (not used yet).

You can also log into a "virtual" account and use that to mess around.

With the tiered pricing it is not that expensive, and for my uses cheaper than DEGIRO would be (if it had the trusts I wanted!).0 -

Lamar Thoughtless Napkin wrote: »Opened an account with Interactive Brokers today, seemed very painless, ID etc. approved in minutes. Transferred a grand in to get started (from Revolut) which may take a couple of days to reach my IB account.

Soured on Trading212, just taking too long to open to new members (guaranteed they will start accepting new members any second now!) and when I considered their FX fees, and lodgement fees (from a Card) as well as other factors discussed previously (share lending etc.) I decided to just bite the bullet and go with IB. I will let people know how I get on, it seems very good so far, oodles of information. There is an online portal for simple trades (will use this most often I'd say) and there is also a "workstation" that you download, this seems very complicated and something like you see day-traders use. There is also a mobile app (not used yet).

You can also log into a "virtual" account and use that to mess around.

With the tiered pricing it is not that expensive, and for my uses cheaper than DEGIRO would be (if it had the trusts I wanted!).

I'd suggest trying the Trader Workstation, it's not overly complicated (even I can use it somewhat), download it anyway and have a look0 -

-

Money hit my IB account first thing this morning. Very impressed with IB, took less than 24hours to get approved, set up and funded.Lamar Thoughtless Napkin wrote: »Opened an account with Interactive Brokers today, seemed very painless, ID etc. approved in minutes. Transferred a grand in to get started (from Revolut) which may take a couple of days to reach my IB account.

Soured on Trading212, just taking too long to open to new members (guaranteed they will start accepting new members any second now!) and when I considered their FX fees, and lodgement fees (from a Card) as well as other factors discussed previously (share lending etc.) I decided to just bite the bullet and go with IB. I will let people know how I get on, it seems very good so far, oodles of information. There is an online portal for simple trades (will use this most often I'd say) and there is also a "workstation" that you download, this seems very complicated and something like you see day-traders use. There is also a mobile app (not used yet).

You can also log into a "virtual" account and use that to mess around.

With the tiered pricing it is not that expensive, and for my uses cheaper than DEGIRO would be (if it had the trusts I wanted!).

One thing to be careful of is that by default the pricing structure seems to default to "fixed" rather than the cheaper, for my uses (and most people I would think) tiered pricing plan. Having changed to tiered in the account settings, this will not take effect until the next working day, so no stock buying for me today!

They offer a virtual "paper" facility so I will play around with that. Have been looking at the Trader Workstation, it is actually easy enough to use, I will have no need for 90% of the functionality of it, but it does seem more stable than the web based client (although that could be my browser).0 -

Lamar Thoughtless Napkin wrote: »Money hit my IB account first thing this morning. Very impressed with IB, took less than 24hours to get approved, set up and funded.

One thing to be careful of is that by default the pricing structure seems to default to "fixed" rather than the cheaper, for my uses (and most people I would think) tiered pricing plan. Having changed to tiered in the account settings, this will not take effect until the next working day, so no stock buying for me today!

They offer a virtual "paper" facility so I will play around with that. Have been looking at the Trader Workstation, it is actually easy enough to use, I will have no need for 90% of the functionality of it, but it does seem more stable than the web based client (although that could be my browser).

Looking at IB myself to consolidate my accounts, am currently on both Degiro and T212 and have particular things I don't like about both.

So for an individual tiered account you are looking at $10 per month minus commission fees which i assume is another word for transaction fees (hopefully correctly) which are €1.25 to €29 (0.05%) , do you pay anything else?, is the UK and US market pricing data real time or delayed, also do they do year end tax statements for CGT?Have a weather station?, why not join the Ireland Weather Network - http://irelandweather.eu/

0 -

Advertisement

-

It is delayed, 15 mins I believe. You can subscribe to live data (which seems expensive) or you can "pay as you go" for a snapshot of data for a trade.Looking at IB myself to consolidate my accounts, am currently on both Degiro and T212 and have particular things I don't like about both.

So for an individual tiered account you are looking at $10 per month minus commission fees which i assume is another word for transaction fees (hopefully correctly) which are €1.25 to €29 (0.05%) , do you pay anything else?, is the UK and US market pricing data real time or delayed, also do they do year end tax statements for CGT?

For my uses (buying to hold) I don't see why I wouldn't use a free live service like Yahoo or something, to get the figures to inform my purchase and tailor it accordingly - so I have not looked properly at the exact costs of live data and snapshots.

As for reports, there is a whole section where it seems you can generate pretty much any report you can think of. Once I have purchased some shares I will play around with it and let you know what I think, although I will maintain a spreadsheet I have designed for these records. I would be amazed if the report functionality on IB would not suffice by itself for what you want, I just like to have manual backups myself.

As for costs, my understanding is that the $10 (USD this is important) is the headline monthly charge, and that commissions are offset against this. So for example, a UK purchase for me will cost 0.050%, with a minimum of GBP 1.00 (Around €1.20 today, or around $1.40, which will be offset against the monthly $10.00). So my understanding is that if I make a few trades a month the $10.00 will be absorbed. When I have over 100K (ha!!) the $10.00 is waived (it appears to be waived for the first three calendar months). Important to note that if your account balance is under 2k the charge is $20.00 a month. (So I have three months to reach 2k overall which should be easily doable with my planned "top ups", provided everything doesn't go to hell!)

As for other charges (will leave aside "optional" ones like live data) and stuff that there may be for margin, option type things (which I have no interest in) there do not seem to be many:

1. Withdrawal Fees: You get one free one per calendar month, any more than that and there is a fee which varies depending on currency and how you want to receive the money.

2. Archived Statements: There is a charge for these (for ones that are not available through your account. You account goes back 4 years for daily statements, and 5 for annual. Should not be an issue, just print them off yearly).

3. FX fees. I am not exactly sure how this works yet, everywhere says some variation of "very good/low". My base currency is in Euro, most of my trading will be in GBP. I lodged 1k in Euro from Revolut, I will see how the fees work out to convert. If there are in any way substantial I will see if I can preconvert to GBP in Revolut and lodge in pounds to IB and see what happens. It appears the costs for spot currency changes are as follows: 0.20 basis point * trade value, with a minimum of 2.00 USD. I think this charge is also offset against the $10.00 a month, but am not sure, will see in practice. I think DEGIRO charge spot rate plus 0.1% and T212 0.15%

I believe a basis point is 1/100th of 1%.

So IB may be cheaper to exchange, especially if it is a larger sum? Does that sound right? Anyway for IB it looks like around €2 to change €1k to GPB, at what seems a great rate, no idea if that is good or not!

Next week I will see if I can lodge directly in GBP, or some USD, and see if it auto converts to my accounts base currency (Euro) or just arrives as I sent it, thus avoiding any fee.

Hope this was helpful!0 -

Thanks very much for that brilliant detailed reply, thats super helpful

")

Have a weather station?, why not join the Ireland Weather Network - http://irelandweather.eu/

0 -

Investment Trusts

Some have found what I have posted previously a help, so I thought I would elaborate more on the subject of Investment Trusts, the ones I have picked, and why. Again the caveat that while I have done some research, I am very much a newbie at this, don't take anything I say, especially opinion, as gospel. I am just saying what I am doing, and why. Ask me in ten years if I was more right than wrong!

The "safest" way for lay people to invest may be in funds/ETFs. These are basically instruments that track an index. So for example you might invest in one which tracks the S&P500 (The biggest American companies, as an EU citizen you can't really invest in this but anyway) so as the market goes up or down so does your ETF. You can just buy it and leave it to do its business, you don't need to keep an eye on things the way you would if you invested in a particular company. However there is a major problem with this strategy, namely the Irish tax laws, specifically "deemed disposal". Basically, every 8 years you have to pay a tax of 41% on any growth/profits and the same rate on exit.

This tax rate is pretty crippling, and certainly damages compounding.

Investment Trusts are the next best thing (and better in some ways). Basically, Investment Trusts are closed end funds, sort of holding companies that are actively managed by a board etc. There are lots of different types with different priorities and philosophies. The manager, depending on the rules of the Trust, can invest in a whole range of things, from shareholdings in particular stocks to bonds, commodities, cash, real estate etc. Most will either use or have the option of using "gearing" (borrowing/leverage). These ITs often have a base index they aim to "beat", which many ITs have a great record of doing. If your IT manager is good/lucky you can make very good gains above what you might in a comparable index, obviously the opposite applies too. Many pay good dividends. The downside is that the company charge a higher fee (usually) from the assets under control than happens with open ended funds/ETFs, but this would seem to me to be a small quibble, especially as IT's are treated, tax wise, the exact same as regular stocks. That is, you pay income tax as normal on dividends and the normal Capital Gains Tax when you sell. This is a massive advantage in two ways: CGT is 33% (less than for an ETF) and if you make a loss you can carry it forward and offset it against any future Capital Gain you may have. You cannot do this if you make a loss on an ETF.

I have checked the tax status of IT's in some detail. Revenue have never said that they should be treated the same as regular stocks. In practice they are. In theory, Revenue could change the rules and say they should be subject to deemed disposal, but this is very unlikely for two reasons: The first is that tax is being paid on an ongoing basis on any dividends. Secondly, is the way in which the IT's trade, they are subject to a premium or discount.

Premium and Discount

This is a very important factor to be aware of. IT's have a Net Asset Value (NAV) which is the real world value of their holdings. So lets say an IT owns only ten stocks, the entire value of which on the open market is £1,000,000. The value of the IT share that you buy on the stock market is not necessarily reflective of that value. Lets say it has ten shares, you would think that the value of the share would be £100,000. But not necessarily. The shares of the IT can trade at a premium or a discount to the NAV. So in our example the shares might trade at £90,000 or £110,000 giving it a discount/premium to NAV of -/+ 10%.

This means there is a great opportunity to essentially pick up shares for less than they are worth now and money can be made if the discount to NAV narrows, even if the underlying value of the shares the IT holds stay the same. You could also "overpay" by buying at a premium. You might think this sounds straightforward, and you should just buy whatever has the biggest discount and don't buy anything at a premium. No, not so fast, you need to investigate. There are often very good reasons for there to be a discount or premium. The NAV is not static, and can go down as well as up.

That said, sometimes discounts are caused by market panic over short term issues, so you can pick bargains up here.

There is also great opportunity (which appeals to me) to pick up particularly good bargains by buying Value orientated IT's at a discount to NAV. In theory, if I buy one of these at a discount, I am buying a company that has made investments that it felt were at a "discount" to their real worth, so I am getting a "double discount" which could give me great returns.

Some ITs try to make sure there is no or a very small premium or discount to NAV. They do this by issuing more shares when there is a premium, and buying shares back when there is a discount.

On the subject of investing styles (lots of variations I am being simplistic here):

Value Investing: Investors with this philosophy (put simply and in general) basically try and figure out the intrinsic value of a stock, and buy it if the market price is significantly below what the investor thinks the Intrinsic Value is. This Intrinsic Value calculation is usually based on fundamentals of a company, incorporating discounted cash flows. The idea is that the rest of the market will eventually figure out that the company is worth more than it is trading at, and the price will increase. This is the old-school approach to investing, the type of which Warren Buffet and co have famously used.

Growth Investing: This is basically investing in companies (often new or small) that have great potential to grow rapidly. TESLA and new tech companies I suppose are examples of this where loads of people have made massive amounts of money. This is the style of investing that has been the most successful in recent years (by a good margin).

Portfolio Picks and Rationale

I have tried to put together a balanced portfolio, in terms of geography, philosophy and investment areas/types. Some might find it helpful to put up a little more about the ITs I have picked, and why.

1. CGT

Capital Gearing Trust defines its objective as follows:

To preserve the real wealth of shareholders and to achieve absolute total return over the medium to longer term through investment in quoted closed-ended funds and other collective investment vehicles, bonds, commodities and cash.

Basically, I picked this as CGT has very low volatility, and weathers storms pretty well. This is a defensive investment which while it won't achieve massive growth, should the market go south it should protect my investment better than most. I am classifying this as "low risk" as per my risk appetite. Currently trading at a typical small premium and produces a dividend yield of 0.54.

2. RICA

Ruffer Investment Company defines its objectives as follows:

The principal objective of the Company is to achieve a positive total annual return, after all expenses, of at least twice the Bank of England Bank Rate by investing predominantly in internationally listed or quoted equities or equity related securities (including convertibles) or bonds which are issued by corporate issuers, supranationals or government organisations.

Another defensive pick, but a little different. This has somewhat of a Value tilt, and, amazingly, actually increased in value in March of 2020 when everything else was collapsing. Again the aim here for me is modest growth in good times, and protection of my investment in bad. Another "low risk". Currently trading at a premium of around 4% and produces a dividend yield of 0.66.

3. TMPL

Temple Bar Investment Trust defines its objectives as follows:

To provide growth in income and capital to achieve a long term total return greater than the benchmark FTSE All-Share Index, through investment primarily in UK securities. The Company's policy is to invest in a broad spread of securities with typically the majority of the portfolio selected from the constituents of the FTSE 350 Index.

I went back and forth on this one. It preformed horrendously during Covid, but since the company replaced its manager it has rebounded very well. This is a committed Value style trust, concentrating on the UK. I think the UK is very undervalued at the moment and there are great opportunities over the long term. I have included this as Value style trust, and for UK exposure. It is currently trading at a small discount of around 2% (it was 15 not too long ago!) and produces a dividend yield of 3.35.

4. AGT

AVI Global Trust defines its objectives as follows:

Established in 1889, the Company’s investment objective is to achieve capital growth through a focused portfolio of investments, particularly in companies whose shares stand at a discount to estimated underlying net asset value.

Unique

A concentrated portfolio combination of family-controlled holding companies, closed-end funds and asset-backed opportunities, unlikely to be found in other funds or indices.

Diversified

A concentrated portfolio of high conviction ideas, yet with broad diversification to sectors and companies through the holding structures of the portfolio companies.

Engaged

Seeking out good quality companies and engaging to improve shareholder value.

Active

Finding complex, inefficient, and overlooked investment opportunities.

Global

Bottom-up stock picking that is benchmark agnostic – seeking the best equity opportunities across the globe.

This is a bit of a different one. It is a Value style, that has a good amount invested in family holding companies. Potential for a very diversified investment here, with a substantial "double discount" as AGT is trading at a current discount of 9%. Current dividend yield is 1.8.

5. MNKS

Monks Investment Trust defines its objectives as follows:

The Trust aims for long-term capital growth which takes priority over income. This is pursued through applying a patient approach to investment, principally from a differentiated, actively managed global equity portfolio containing a diversified range of growth stocks – companies with above average earnings growth – which we expect to hold for around five years on average. Investments are made on an unconstrained basis. The portfolio, which includes stocks with a range of different growth profiles, will typically contain 100+ stocks from around the world and Monks should not be viewed as a proxy for any index.

Went back and forth over whether to pick this or its stablemate Scottish Mortgage (SMT). Both are Growth style, SMT has better historic performance (although MNKS is no slouch). What settled it is that too much of SMT is unlisted investments, and it is too top heavy in stocks like Tesla. MNKS is a bit of a watered down version of SMT with less volatility. I included MNKS in my portfolio as a Growth style investment, riskier but may provide higher returns than others in my portfolio. Currently trading at a small premium of around 2% and has a dividend yield of 0.18.

6. JMG

JPMorgan Emerging Markets IT defines its objectives as:

This Company aims to maximise total returns from Emerging Markets and provides investors with a diversified portfolio of shares in companies which the manager believe offer the most attractive opportunities for growth. The Company can hold up to 10% cash or utilise gearing of up to 20% of net assets where appropriate.

Another growth style, this time with focus on China and emerging markets which I wanted exposure to. Higher risk than some others, but could provide handsome returns. Has a current dividend yield of 1.07.

7. PCT

Polar Capital Technology Trust defines its objectives as:

Polar Capital Technology Trust plc provides investors with access to the potential of companies in the global technology sector. Managed by a team of dedicated technology specialists, PCT has grown to become a leading European investor with a multi-cycle track record – a result of the managers’ approach to investing, with the ability to spot developing technology trends early on and to invest in those companies best placed to exploit them.

Another Growth IT, it has provided amazing returns over the past few years. Included this as I wanted dedicated Tech exposure. Went back and forth on PCT vs ATT but because PCT is more geographically diversified and trading at a discount of around 8% below NAV I decided on PCT. A riskier investment, but should tech continue to boom it could continue to provide fantastic returns. Provides zero dividend.

8. BRK.B

About:

Berkshire Hathaway, Inc. engages in the provision of property and casualty insurance and reinsurance, utilities and energy, freight rail transportation, finance, manufacturing, and retailing services. It operates through following segments: GEICO, Berkshire Hathaway Reinsurance Group, Berkshire Hathaway Primary Group, Burlington Northern Santa Fe, LLC (BNSF), Berkshire Hathaway Energy, McLane Company, Manufacturing, and Service and Retailing. The GEICO segment involves in underwriting private passenger automobile insurance mainly by direct response methods. The Berkshire Hathaway Reinsurance Group segment consists of underwriting excess-of-loss and quota-share and facultative reinsurance worldwide. The Berkshire Hathaway Primary Group segment comprises of underwriting multiple lines of property and casualty insurance policies for primarily commercial accounts. The BNSF segment operates railroad systems in North America. The Berkshire Hathaway Energy segments deals with regulated electric and gas utility, including power generation and distribution activities, and real estate brokerage activities. The McLane Company segment offers wholesale distribution of groceries and non-food items. The Manufacturing segment includes industrial and end-user products, building products, and apparel. The Service and Retailing segment provides fractional aircraft ownership programs, aviation pilot training, electronic components distribution, and various retailing businesses, including automobile dealerships, and trailer and furniture leasing. The company was founded by Oliver Chace in 1839 and is headquartered in Omaha, NE.

This is not an Investment Trust. Berkshire should need little introduction, it is Warren Buffet's holding company. As detailed above it directly owns some amazing companies, and also holds stocks of a number of others. I included this for more concentrated exposure on US companies, with a Value style. It has huge cash reserves which is attractive too. Currently I think it is a bit undervalued, evidenced not least by continuing massive buybacks. Over the long term I hope it will continue to deliver modest to decent returns, and be less volatile than some, particularly in a bear market. It provides no dividend.

Obviously anyone thinking of investing in these should do their own research. I found the annual reports, and videos of annual briefings really helpful, as well as a few podcasts with interviews of the relevant investment managers.

Regarding my portfolio, I may add positions in certain individual companies, or add more ITs over time (particularly in specialist areas) but I see no reason why I should have to remove (barring something exceptional happening or a new better player arriving on scene) any of my holdings (I want to make as few CGT returns as possible!). I think this portfolio gives me a very good chance of achieving my goal, which is to make more on my money than if I just stuck it into the bank. I know it means little, but if I had this portfolio over the past five years I would have absolutely smashed that objective.0 -

Just to add, the most user friendly site I found to track IT's, including discount/premium is https://www.trustnet.com/. You can set up a watchlist, alerts etc. All for free.0

-