Only a policyholder can claim indemnity from an insurance policy. In this instance, the 3rd party claimed for funds under their policy to allow them compensate you for the loss they were responsible for

Haven't a clue what that means tbh...

56yrs / Full DL / No claims / No PP / BYD Seal RWD.

Lasy year with BOI (with RSA as u/writer) was €597. Renewal at €757. Called and they reduced renewal to €682. Off to waste more time on the merry hunt. Absolute bollox from Chill as a starting point.

Renewing for a 2018 Passat estate - Comfortline with no modifications. Early 30's with 6 years full Irish licence, no points, offences or claims. Now I've only 3 year's NCB as I only bought my first car in 2022, but was still a named driver on a relative's policy up to then.

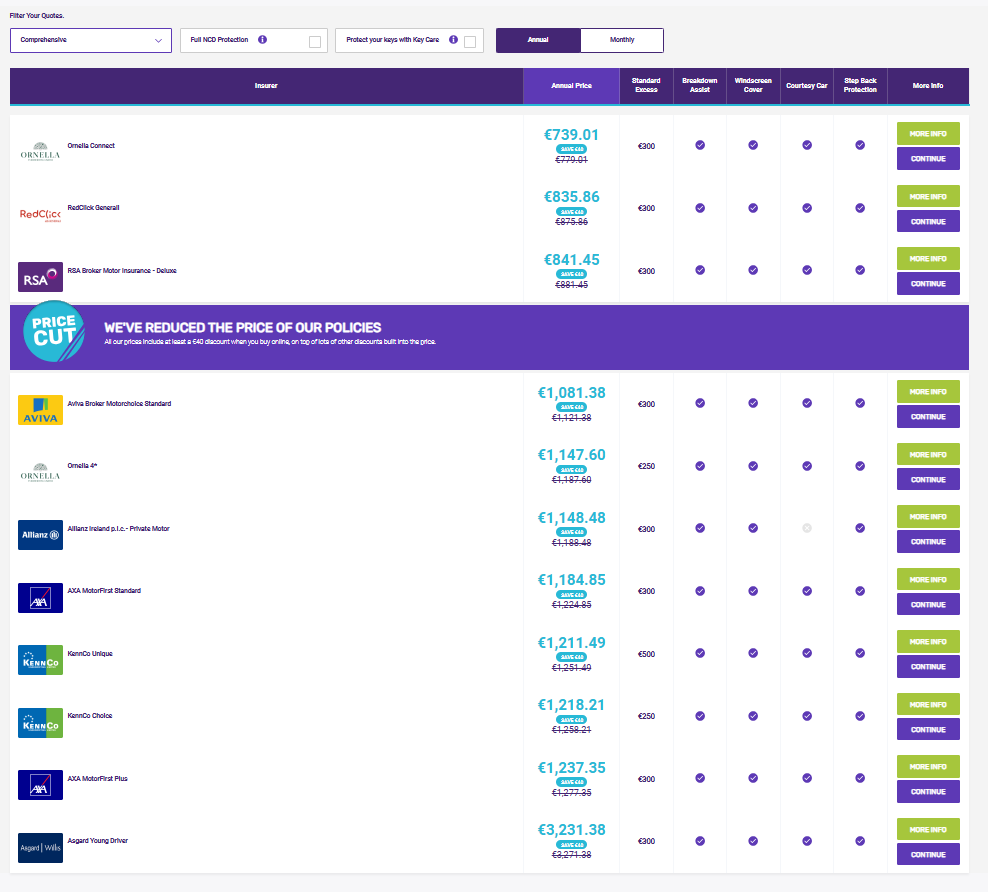

Further details such as adding the OH onto the renewal gave the below quotes online:

No improvements to any quotes when ringing. Chose AXA in the end as I was with them before, had good customer experience and seemed to offer more than RedClick, but adding 24/7 breakdown cover bumped it to almost €700. Felt worth it for the peace of mind since I do long distance drives quite often at unsocial hours.

But didn't have many reasonable options this year really, so not very happy is putting it mildly. For whatever reason it seems the Passat is the problem. Showed the quotes to friends, colleagues and the OH, many with the same circumstances, age bracket and similar vehicles (e.g. Skoda Superb, Golf R, 530d) and I don't think any of them were given quotes above €500 on the first try, let alone be refused from several. Meanwhile I couldn't even get a quote from Revolut.

If you were rear ended & deemed not at fault why is there a claim against your insurance policy? Was the other driver not insured or what?

Age: 35 male

Car: 142 Kia ceed 1.4 petrol

Insurance: Zurich

Last year: €389

This year: €371

Have been very lucky with Zurich over the years. Will call and try reduce it but fine to stick with that. Just tried FBD so far and quoted €452.

Male 46

Full NCD

Last year €350, Aviva via AA for TPFT

Best this year Aviva via Chill, €364 for fully comp with all the bells and whistles.

2010 Hyundai i30

Male, age 51

Full NCB for as long as I can remember.

Full license for 25 years.

Last year I paid €459 with the AA on a 2021 BMW i4. This year, the renewal jumped to €698.

Doing the usual quotes merry-go-round and most are coming in around the same. Parasites!

Male, 49, Full NCB for as long as Im driving, Full Lic for over 25 years

Volvo v60 2.4D, Last year 480

Renewal quote from Allianz -580, includes other cars, full comp, 250 excess, full NCB protection

Aviva - 765

AA (Allianz underwrite) - 780+

Zurich - 780+

Chill - min 800

Campion - 900+

Seems I can't get insured with anyone else except Allianz, the + denotes that these didn't include ncb protection or other add ons.

Have tried Allianz as new customer but get the same quote…..

Outsurance just came in with 370 - but no NCB protection. Is it worth the risk for the year(Allianz @ 570)?

In my option the Outsurance model is for risk takers. I didn't go with them because of the lack of NCB protection. The loss of your NCB will cost many times the €200 savings over several years until you have built your NCB again.

I’ve just closed a claim from last year when I was hit be an uninsured driver. Got the car repaired on my own policy as advised. Have just had the excess returned, and have a letter to explain that the MIBI protocol was applied. NCB is unaffected, but I’ll have to declare the incident (with the MIBI explainer) gor 5 years from the accident. Actually felt a bit dirty for the other driver. We swooped details at the time, and I think she genuinely believed it had been told she was insured on the car she was driving. Now it’s clear why the partner seemed so frantic to fix things privately. MIBI protocol takes longer than a straightforward claim, but I am happy with the outcome. Details below. Make sure to get the reg! Nothing happens without it!

https://www.mibi.ie/making-a-claim/uninsured-vehicles/

I went with them €327 compared to over €600 with any of the others, maybe I'll regret it, who knows?

Still don't get why the regulator doesn't just force the insurance companies to allow us to use the same portal to compare quotes. Like what they have done for health insurance. https://www.hia.ie/health-insurance-comparison

It's not like they don't have incompatible systems. They all use the same claims database, insurance link and the government driver license and car registration, National Vehicle and Driver File.

I also don't get why they force you to ring up sometimes. They put the same information in to a computer and instantly give you a quote. It's not like they had to walk over to their manager and ask for an actuary's opinion.

I went with them but then pulled out😂

The risk of losing the NCB protection would just grate me so will pay the 200 difference just for peace of mind! Such a coward🙈

To be perfectly honest I didn't have 600 odd to spend on insurance, I was investigating who the best company were to go with for paying monthly which I haven't done in years, luckily I didn't need to do it in the end. Next year will tell the story I suppose…

Paying monthly is considered a risk, so your premium is increased.

Also a nice little earner for insurance companies as it probably bumps up the total paid by €50+

Been with Bank of Ireland (RSA) paying monthly because no interest added for a good few years, quotes reasonable, saying that Bank of Ireland no longer doing car insurance from next year, but RSA will still quote apparently.

AIB don't charge extra, deposit and the rest over 9 months, luckily I didn't have to go that route.

I’m changing my car today from a 231 ID4 to a brand new ID4, my policy expires in December. I am with Invernia through Chill. They have just charged me €183 to change. I am still in the floor, absolutely staggered. They had me over a barrel as I had to do it but will certainly be lodging a complaint. My policy for the year cost around €500 when I renewed last December.

€183 for 3 months is madness. If you are through a broker, the charge will be made up by a combination of the broker fee and what Invernia, as underwriters, are charging. Ask for the original endorsement from Invernia noting their additional premium and read your brokers Terms of Business booklet for their fee structure

Eff that caper when it's already paid, just shop around in December. EVs seem to be getting big hikes in the insurance premiums.

If the charge is not in line with their terms of business and you don't challenge them on it, they will continue to do it for the next person

Would assume the charge is made up of an admin fee for the change plus the upgrade of the car type. It's hard to know what's reasonable, but I would have guessed ballpark 100 yoyos.

They have limits they can charge for admin, as laid in the terms of business booklet and they can't exceed them. That's why I suggest you get a breakdown of the underwriters charge and their fee. If the bulk is the underwriter, them you have to take it on the chin and move at renewal

There was a €55 admin charge for Chill to which they have refunded €30 as a sign of goodwill!!! No movement from Invernia. Newer car, value now €44k from €30k. Will try to get a breakdown of the Invernia charge then will be shopping around when renewal comes in

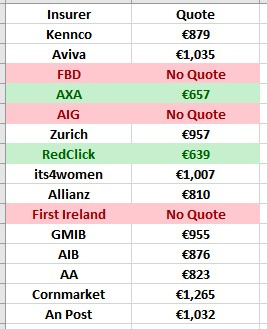

Currently doing the insurance shop around. With 123.ie at the moment, they wanted 548 to renew. Checked as a new customer and it was 546,

Car is 2020 BMW 330e, 20+ years driver licence and no claims.

All below quotes have ncd protection added

Aviva

536

AIG

649

GetSetGo

440

AXA

769

123.ie

548 renewal; 546 new cust

AA

668

FBD

607

Allianz

870

Supervalu

787

Liberty red click

643

Zurich

591

An Post

596

Its4Women

434

KennCo

805

So will double check getsetgo and its4women for the benefits and ring 123 to see can they match.

Some of these companies need to update their job role lists.

And for many years now AXA, KennCo, Allianz are always at the top end, I know it differs person to person but can't see how they compete?!

Thanks @ilikeboats - who did you end up going with. I've just received a few quotes and Itsforwomen definitely standing out from the rest… They will charge me additional €25 for indemnity letter for employer… Still under the other quotes..

Insurance up soon but getting ridiculous quotes. In my thirties, full no claims, never had penalty points or accidents. Paid €390 2 years ago, around €600 last year and now this year the cheapest quote is €710! Sick of insurance in this country. Only thing that changed is I bought a 2017 audi a6 this year, are they heavily loaded or something?!