2Mad2BeMad wrote: » Ya I plan on retiring at 30, im 26 now and havn't saved a penny into a pension yet, but if i manage to stick 5 percent of my annual income into it at which my employer will match by 100000% i reckon il have at least 45million by then. Not sure if its enough though might have to stretch it to 35. I'll see.

KyussB wrote: » A good rule of thumb, is that anyone promising you growth significantly greater than the percentage of GDP growth, is a con man.

high_king wrote: » That's ok . . If that's how they want to play it . . I'll just milk the system instead as well then.

S.M.B. wrote: » Is auto enrollment not a necessary step to manage the massive move from Defined Benefit pensions to Defined Contribution pensions as opposed to the first step in a grand plan to means test the state pension?

Wanderer78 wrote: » if your not of pensionable age, you wont be receiving it, and you ll also find it difficult to pick up work in your 60's

Henry Ford III wrote: » Non contrib. OAP is already means tested.

Squozen wrote: » The US stockmarket has given significantly greater returns than their GDP growth for the last century.

Dodge wrote: » I think what this thread highlights is the need for some sort of automatic enrolment pension scheme to be honest The amount of people who clearly have no idea how pensions work now, never mind how they may work in the future, is ridiculous If you want to have any sort of good living standard when you retire, you need to start saving for it. If all the launch of auto enrolment does is make people aware of that, even if makes them have a look at what products are available, then it will be a success

high_king wrote: » It's this type of half witted patronising shyte that FG are famous for.

BailMeOut wrote: » Can you please explain what you mean by this?

KyussB wrote: » The reason the government can't be relied on this way, is due to the NeoLiberal ideological leanings of the main parties - enacting stupid shit like this massive auto-enrollment subsidy of the finance industry...

KyussB wrote: » Government properly funding publicly provided pensions is nothing more than a political decision - if it's a priority to the government, it can be done perfectly sustainably. The reason the government can't be relied on this way, is due to the NeoLiberal ideological leanings of the main parties - enacting stupid shit like this massive auto-enrollment subsidy of the finance industry...

Mantis Toboggan wrote: » 20% of people die in Ireland before they reach 65 so I'd slightly agree with the OP, chances are you'll never see that money. Life is short, enjoy it, we'll all be dead in 80 years anyway and a few years dead and you're long forgotten.

KyussB wrote: » The stock market is incredibly volatile, and the rate of return depends upon how selectively you pick your start and end dates - someone who isn't looking to be conned, should expect only a small number of percentage points return, above GDP growth - at best.

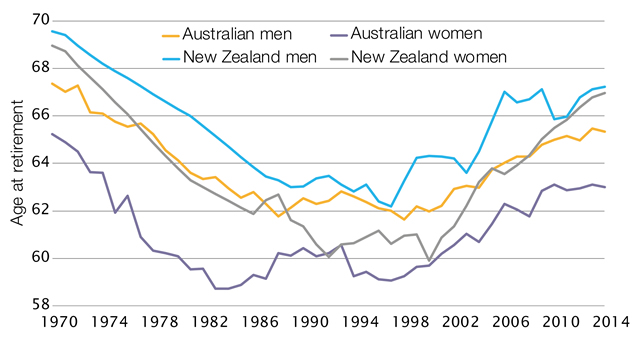

Squozen wrote: » And again I’ll point out that Australians retire at the age of 55 due to this ‘stupid ****’.

Jim2007 wrote: » You don't have to be a genius to figure out that the population is getting order and that in 50 years time there simply will not be enough people around to pay for your pension and those that are in the workforce will not want to hand over say double or more the current social security rate just so you can have a pension and good social services to look after you in old age. You are right politicians do what get's them elected, that is why it has taken so long right a cross Europe for them to bring home this bad news. And by the same token don't expect voters in 50 years time will be voting for politicians that will increase their taxes to cover your pensions and other social needs, they will not.

Jim2007 wrote: » A better rule of thumb is that when you don't know what you are talking about, you research the topic using actual facts rather than listen to the political blah, blah... The majority of pension funds across Europe regularly deliver returns of between 4% and 8% and do so at reasonably risk levels. I know this because I spent 30 years doing performance and attribution analysis on about a 1000 of them.

mydingaling2 wrote: » Currently paying 15% of my salary into a 401K pension with the employer matching 8%. I can withdraw whenever I like but plan on retiring at 55 and going home permanently. I can take it at 55 if im still with the same company and before this i'm hit with a 10% penalty. I only started paying in at age 28. This is what my pension will look at going by years. Age 35: 143K Age 40: 307K Age 45: 548K Age 50: 899K Age 55: 1,404,000 Age 60: 2,127,000 Age 65: 3,158,000 I am taxed on whatever i take out. I know that I am secure with the rest of my salary once i am paying into the pension but still manage to save 1200 a month out of my main salary without the pension. Thinks could change and I might plan on retiring at 50 and heading home and have my savings and pension as a nest egg.

KyussB wrote: » Public pensions are meant to be paid by the public purse - they don't suffer any of the effects of demographics, unless they are deliberately designed to for political reasons.

KyussB wrote: » You don't understand how government finances work - public funding doesn't come 1:1 from taxes, and your speaking as if it does - it almost never does.

KyussB wrote: » There you are parroting the idea that government spending comes 1:1 from taxes again... The demographics timebomb is certainly going to be a thing for privately managed pension funds, yes - that's why we need to bolster the safety net of the public pension, which has no such problem. Budgets aren't funded 1:1 from taxes - almost never. Balanced budgets almost never happen.

![Photo of [Deleted User]](https://www.boards.ie/applications/dashboard/design/images/banned.png)

![Photo of [Deleted User]](https://w7.vanillicon.com/v2/761dc761e98b4e4a2ae41c6abf8a928b.svg)